The Investment Banking Stack: How to Run Deal Materials with Claude

How investment banking analysts and associates use Claude Code skills across the full deal lifecycle — from teasers and CIMs to merger models, LBOs, and comps.

An M&A deal produces a lot of documents. The teaser, the CIM, the buyer list, the process letter, the pitchbook, the financial model, the data room pack — each one takes time, follows a defined structure, and needs to be consistent with everything that came before it. In a live process, the timeline doesn’t accommodate starting from scratch on any of them.

The Investment Banking Stack gives Claude a structured approach to each of these deliverables. Each skill knows the format the document needs to take, the sections that belong in it, and the level of detail that buyers, sellers, and counterparties expect. The starting point is always strong, which means the time goes into getting the substance right — the company’s story, the model assumptions, the buyer rationale — rather than reconstructing the skeleton from a prior deal that’s close but not quite right.

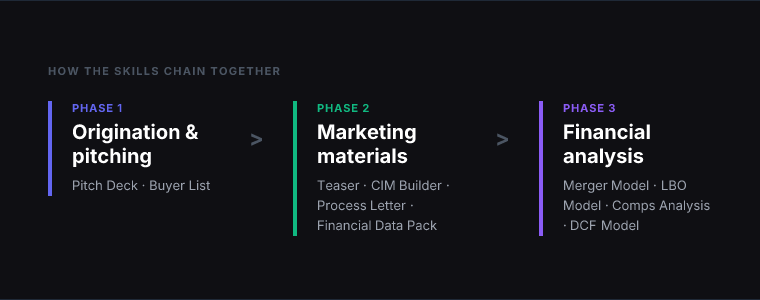

The stack covers the full deal lifecycle: origination and pitching, marketing material production, and the financial analysis that underpins every deal. The skills work independently — you don’t have to use all of them or use them in order. Most analysts find themselves reaching for different skills depending on where they are in a process, and sometimes returning to the same skill multiple times as a deal evolves.

The deal lifecycle, skill by skill

Origination and pitching

Pitch Deck builds pitchbooks for new business development — credentials, market overview, deal experience, and the fee and process recommendation that wins mandates. A new business pitchbook has a specific job: convince a potential client that you understand their situation, have relevant experience, and have a credible view on how to run the process. The structure matters as much as the content. The Pitch Deck skill produces an organised starting point that covers all the sections a client expects — market positioning, deal type expertise, comparable transactions — and presents the fee and timeline recommendation in the sequence that leads to a yes.

When you’re in front of a potential client, the deck does the selling. Use it when building a pitchbook for a sell-side or buy-side mandate, or when refreshing your credentials for a sector where the bank is actively pursuing new business.

Buyer List develops qualified acquirer universes for sell-side processes — strategic buyers, financial sponsors, and the rationale for each. A well-constructed buyer list is one of the most client-facing early deliverables in a sell-side mandate: it tells the client who’s likely to pay, why, and how you plan to sequence outreach. A list that’s too narrow leaves money on the table. A list that’s too broad signals that no real work went into it.

Use it to structure the buyer universe conversation before outreach begins, or to pressure-test a list you’ve already drafted against the universe of strategics and sponsors who might have a legitimate interest.

npx skills add anthropics/financial-services-plugins --skill investment-bankingMarketing materials

Teaser writes anonymous deal teasers — company overview, investment highlights, and the brief format that gets a qualified buyer to sign an NDA without revealing the seller’s identity. The output follows the standard one to two page format that buyers expect: enough to evaluate whether the opportunity is worth pursuing, not enough to identify the company without signing. The most common mistake with teasers is either including too much detail (which narrows the universe of interested parties and reveals too much before NDAs are signed) or too little (which doesn’t generate enough interest to get buyers to the table).

Use it when beginning a sell-side process, when the client’s business is complex enough that framing the investment thesis clearly matters, or when you’re running a broad process where the teaser needs to generate responses across a wide range of buyers.

CIM Builder assembles comprehensive information memoranda — company overview, industry context, historical financials, management team, and the detailed narrative that gives buyers what they need to submit a preliminary bid. The CIM is the most time-intensive marketing document on any sell-side process, and the one where structure matters most. A well-built CIM moves buyers efficiently from curiosity to a serious bid. A poorly organised one slows the process and creates the impression that the seller isn’t ready.

Use it to structure the CIM drafting process from scratch, or to reorganise an existing draft that’s grown unwieldy as sections were added under deadline pressure.

Process Letter drafts bid instructions, IOI guidelines, and process letters — the procedural documents that manage buyer access, set timeline expectations, and define what a qualifying bid looks like. These documents feel routine but the details matter: an ambiguous bid instruction produces inconsistent submissions that are hard to compare. A process letter that doesn’t set clear expectations for management access creates friction at a critical stage.

Use it when a process is moving from NDA to first-round bids, or when the timeline needs to be formalised and communicated to all parties simultaneously.

npx skills add anthropics/financial-services-plugins --skill investment-bankingFinancial analysis

Financial Data Pack Builder compiles the financial content for a data room — historical financials, adjusted EBITDA bridge, working capital analysis, and the structured presentation that buyers use for diligence models. The data room is where a deal gets stress-tested by buyer diligence teams, and the quality of the financial data pack determines how smoothly that process goes. Missing schedules, unexplained adjustments, or inconsistent periodicity all generate questions that slow the process.

Use it to structure the financial data package before a data room opens, or to review an existing data pack for completeness before the first round of buyer diligence begins.

Merger Model builds merger and accretion/dilution models — transaction assumptions, synergy phasing, combined P&L, and the sensitivity tables that show how deal economics shift under different scenarios. The A/D model is a standard deliverable for buy-side analysis and often forms the quantitative backbone of a CIM’s financial section. Getting the model structure right — particularly the synergy treatment and the share count arithmetic — matters more than most analysts expect when they first build one.

Use it when a client is considering an acquisition and needs to understand the earnings impact, or when building the financial analysis section of a CIM that needs to show buyers what the combined entity looks like.

LBO Model structures leveraged buyout analysis — debt capacity, returns at various entry multiples, management incentive modeling, and the scenario analysis that underpins sponsor bids. LBO analysis is the sponsor universe’s primary valuation tool, and it’s also useful on sell-side processes for anchoring expectations about where financial buyers are likely to bid. The model needs to be right on the debt structure and return mechanics, and the sensitivity tables need to cover the assumptions that sponsors will push on in negotiation.

Use it when preparing financial analysis for a sale process where sponsor interest is material, or when advising a client who is evaluating inbound acquisition interest from financial buyers.

Comps Analysis runs comparable company and precedent transaction analyses — peer selection, multiple calculation, and the valuation summary that anchors a fairness opinion or pitchbook valuation section. Comps are the most visible part of a valuation analysis and the one that generates the most questions from clients. Peer selection methodology, which multiples to use, and how to handle outliers all require judgment — the skill handles the structure and calculation framework so the analysis time goes into those decisions rather than the spreadsheet mechanics.

Use it when building a valuation section for a pitch or CIM, or when the engagement requires a formal fairness opinion where the comparable company and transaction analysis needs to be defensible.

DCF Model Builder builds discounted cash flow models — projection build, WACC derivation, terminal value methodology, and the sensitivity tables that show how valuation changes with key assumptions. The DCF is the most assumption-sensitive valuation methodology, which means the model structure needs to make the key assumptions visible and the sensitivity analysis needs to cover the inputs that drive the most variance in output.

Use it when building a standalone valuation model, when the engagement requires a DCF alongside comps for a full valuation analysis, or when a client wants to understand how their business value changes under different growth and margin scenarios.

npx skills add anthropics/financial-services-plugins --skill financial-analysisHow the stack works together

The skills follow the natural deal sequence. In a sell-side process, the timeline typically looks like this:

Mandate stage: Pitch Deck and Buyer List come first — the pitchbook wins the mandate, and the buyer list frames the process strategy before outreach begins. These two skills inform each other: the buyer rationale in the buyer list is often the basis for the deal positioning in the marketing materials that follow.

Marketing stage: Teaser, CIM Builder, and Process Letter run in parallel once the mandate is live. The teaser goes to market first; the CIM is under construction simultaneously. Financial Data Pack Builder feeds into the CIM’s financial section and the data room that opens after NDAs are signed.

Analysis running throughout: Merger Model, LBO Model, Comps Analysis, and DCF Model Builder support both the marketing materials and the buy-side analysis that happens once buyers are in the process. On a sell-side mandate, comps and the DCF anchor the management presentation. LBO analysis frames expectations about sponsor interest. On a buy-side mandate, the merger model and LBO model are the primary analytical deliverables.

No skill assumes you’ve used another — each triggers independently based on what you ask for. Most analysts use the deal document skills and the modeling skills in parallel rather than sequentially, which is how live processes actually run.

The install command is the same for the deal document skills (--skill investment-banking) and a different path for the modeling tools (--skill financial-analysis). Both come from the same source repo.

Install the full stack

→ View the Investment Banking Stack

Browse all finance skills → /audiences/finance

📬 Weekly digest

Get the best new skills every Tuesday

3–5 hand-picked skills. Free forever.

More guides

April 4, 2026 · 8 min read

The CEO of Y Combinator Ships 10,000 Lines of Code a Day. Here's Exactly How.

Garry Tan runs one of the most demanding jobs in tech. He's also shipping more code than ever. gstack — his open-source Claude Code system — is how. Here's what it is and why it works.

March 25, 2026 · 7 min read

How to Create a Claude Skill (Step-by-Step Guide)

Learn how to build, test, and share your own Claude Code skills. A complete walkthrough — from blank file to installed skill — with real examples and best practices.

March 24, 2026 · 8 min read

Awesome Claude Skills: The Complete Searchable List (2026)

Every major Claude Code skills list and awesome-claude-code repository in one place — with install commands, categories, and a searchable directory for all 370+ skills.